Kenya’s banking landscape is undergoing a dramatic transformation as stringent new capital requirements create unprecedented opportunities for Africa’s largest financial institutions to expand their footprint in East Africa’s economic powerhouse. The regulatory shift, coupled with the exit of smaller players and a government push for consolidation, has positioned Kenya as the premier destination for pan-African banking expansion in 2024 and 2025.

New Regulatory Framework Opens Door for Regional Consolidation

From Lagos to Cairo to Johannesburg, Africa’s banking titans are converging on Nairobi. In just two years, Kenya has witnessed a surge in cross-border acquisition attempts, with Nigerian and Egyptian lenders sealing deals and South African giants now circling. The drivers are clear: ambitious regulatory reforms, expanding market potential, and Kenya’s role as East and Central Africa’s financial nerve centre.

This transformation is much more than a reshuffling of ownership. It is the beginning of a continental banking realignment—one that will reshape competition, accelerate digital disruption, and determine who controls Africa’s fast-growing financial markets.

Key Developments in Kenya’s Banking Consolidation

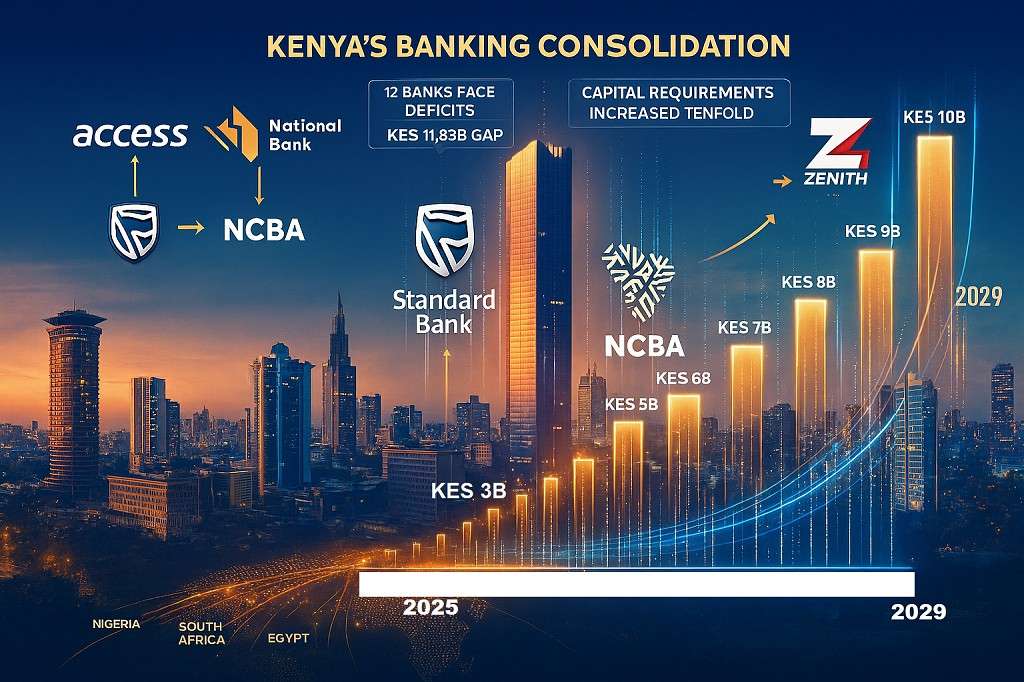

- Capital requirements increased tenfold: Banks must hold KES 10 billion by 2029, up from KES 1 billion

- 12 banks face deficits: Institutions need KES 11.85 billion collectively to meet 2025 thresholds

- Access Bank acquires NBK: Nigeria’s third-largest bank approved to purchase National Bank of Kenya

- Zenith Bank enters market: Plans Paramount Bank acquisition, expanding pan-African presence

- Standard Bank eyes NCBA: Potential merger would create KES 1.1 trillion banking powerhouse

The Capital Requirements Catalyst

In June 2024, the Central Bank of Kenya (CBK) announced a landmark tenfold increase in minimum capital requirements for commercial banks, raising the threshold from KES 1 billion ($7.7 million) to KES 10 billion ($77 million). President William Ruto signed the Business Laws (Amendment) Act in December 2024, establishing a phased implementation timeline that extends to 2029.

Under the new framework, banks must maintain KES 3 billion in core capital by December 2025, KES 5 billion by 2026, KES 7 billion by 2027, KES 8 billion by 2028, and the full KES 10 billion by 2029. This represents the most significant regulatory overhaul since 2012, when the requirement was last adjusted from KES 250 million to KES 1 billion.

Table: Capital Requirement Implementation Timeline

| Year | Minimum Core Capital Requirement | Key Implications |

| 2025 | KSh 3 billion | Initial filter for smaller institutions |

| 2029 | KSh 10 billion | Full implementation driving current M&A activity |

| Previous | KSh 1 billion | Previous standard that allowed market fragmentation |

Source: Central Bank of Kenya

The new requirements stem from mounting systemic risks within Kenya’s banking sector. Non-performing loans (NPLs) surged to 15.7% of total loans in March 2024, the highest level since 2006. This deterioration reflects persistently weak loan growth, elevated lending rates, high inflation, currency pressures, and delays in government payments. Additionally, banks face significant exposure to the public sector, with government loans comprising 29.7% of total loan portfolios as of April 2024.

CBK Governor Kamau Thugge emphasized the climate and cybersecurity dimensions driving the policy shift. The increased capital buffers aim to strengthen banks’ resilience against emerging risks, from cyber fraud threats to climate-related financial disruptions, positioning the sector to support larger-scale infrastructure projects across the region.

But the rule created a second effect: a buyer’s market for foreign banks.

Smaller and mid-tier lenders—many with assets under KSh 50 billion—now face an expensive choice: raise costly new equity, merge with competitors, or sell to bigger players. For well-capitalized pan-African banks in Nigeria, Egypt, and South Africa, the timing could not be better.

Leadership in Financial Inclusion and Digital Innovation

Kenya’s banking sector stands out globally for its remarkable financial inclusion rates, largely driven by pioneering mobile banking solutions. The country’s formal financial inclusion rate has reached 90.1%—the highest in sub-Saharan Africa—up from 79.1% just three years earlier in 2021. This achievement is largely attributable to the successful integration of traditional banking with mobile money platforms, particularly M-Pesa.

Kenyan banks have masterfully leveraged mobile integration and extensive agent networks to extend services to rural and previously unbanked populations. Through partnerships with platforms like M-Pesa, these institutions enable real-time access to loans, savings, and insurance products, creating a deeply embedded financial ecosystem. This digital infrastructure represents a significant competitive advantage and attraction for incoming banks seeking to tap into a technologically sophisticated customer base.

Table: Comparative Banking Sector Performance Across Africa (2025)

| Country | Brand Value Growth | Total Banking Brand Value | Financial Inclusion Rate |

| Kenya | 25.1% | $1.18 billion | 90.1% |

| South Africa | 23.6% | $8.86 billion | 85.4% |

| Egypt | 8.03% | $1.48 billion | Not specified |

| Nigeria | 5.37% | $1.57 billion | 63% |

Source: Brand Finance African Banking Report

Nigerian Banking Titans Lead the Charge

Nigeria’s banking powerhouses have emerged as the most aggressive acquirers in Kenya’s evolving landscape, leveraging their continent-wide expansion strategies and deep capital reserves.

Access Bank’s Acquisition Spree

Access Bank Plc, Nigeria’s third-largest lender, has established itself as the most active player in Kenya’s banking consolidation. In April 2025, the CBK approved Access Bank’s acquisition of 100% of the National Bank of Kenya (NBK) from KCB Group, marking the bank’s second major acquisition in Kenya following its 2020 purchase of Transnational Bank.

The NBK acquisition represents a strategic pivot for Access Bank, which had previously attempted to acquire 83.4% of Sidian Bank from Centum Investments in 2022, though that deal expired without completion. Access Bank’s aggressive regional expansion has seen it acquire 14 banks across Africa, including Standard Chartered’s consumer banking divisions in Tanzania (June 2025), Angola, and Sierra Leone, as well as pending acquisitions of Bidvest Bank in South Africa and AfrAsia Bank in Mauritius.

Access Bank Kenya faces significant capital pressure under the new rules. Based on December 2023 figures, the bank required at least KES 1.5 billion to meet even the initial KES 3 billion threshold, positioning the NBK acquisition as both a growth opportunity and a capital solution.

Elizabeth Oguegbu, Access Bank’s Group Head of Financial Markets & Funding, indicated the bank is now consolidating its pan-African presence to champion intra-Africa trade and financial integration, while embedding fintech capabilities through platforms like Oxygen (payday loans) and Hydrogen (payment services).

Zenith Bank’s Ambitious Entry

Zenith Bank, another Nigerian giant, has confirmed plans to enter the Kenyan market through acquisition. In November 2025, the bank disclosed that it had filed for regulatory approval with both the Central Bank of Kenya and the Central Bank of Nigeria to acquire Paramount Bank, a transaction expected to conclude by early 2026.

Zenith Bank secured $230 million in late 2024 through an oversubscribed rights issue and public offering, specifically earmarked for expanding banking operations across Africa and internationally. Henry Oroh, Zenith’s Executive Director, announced at the Africa CEO Forum 2025 that the bank would expand to Kenya, Côte d’Ivoire, Senegal, and Cameroon in 2025.

Paramount Bank, which traces its origins to 1993 when it operated as Combined Finance Limited, requires approximately KES 521.9 million in additional capital to meet the 2025 threshold. The bank’s capital deficit makes it an attractive acquisition target for well-capitalized regional players.

Zenith’s expansion philosophy centers on creating African banking champions with sufficient scale to serve African businesses without dependence on Western financial institutions. The bank emphasized that Africa’s abundant natural resources and minerals are attracting global attention, necessitating strong African financial institutions to intermediate capital flows.

Standard Bank’s NCBA Pursuit

Africa’s largest bank by assets, Standard Bank Group of South Africa, has emerged as the most ambitious player in Kenya’s consolidation wave. In October 2025, Bloomberg reported that Standard Bank has directed its 75%-owned Kenyan subsidiary, Stanbic Holdings, to pursue acquisition talks with NCBA Group, potentially creating Kenya’s third-largest bank.

The proposed transaction would combine approximately KES 1.1 trillion ($8.5 billion) in assets, positioning the merged entity behind only Equity Group Holdings and KCB Group. NCBA’s shares surged 70.6% following the acquisition reports, with the bank’s market valuation reaching KES 158.5 billion by October 2025.

Standard Bank’s East Africa Regional Chief Executive Patrick Mweheire had telegraphed this strategy in March 2023, stating the bank planned to acquire a Kenyan lender by 2025 as part of its ambition to become a top-three player in its African markets. The timing aligns perfectly with Kenya’s consolidation push, as NCBA brings 121 branches serving 415,000 customers across Kenya, Uganda, Tanzania, and Rwanda, compared to Stanbic’s 30 branches and 310,000 customers.

NCBA’s appeal extends beyond its branch network. The bank was formed through the 2019 merger of Commercial Bank of Africa (CBA) and NIC Group, combining CBA’s digital strength through the M-Shwari mobile banking platform with NIC’s corporate banking and asset finance expertise. NCBA commands a 36% market share in Kenya’s asset finance sector and has maintained consistent dividend payouts, distributing KES 9.06 billion in 2024 and KES 31.2 billion over the past five years.

The families of former President Jomo Kenyatta and former CBK Governor Philip Ndegwa hold significant stakes in NCBA, controlling 13.2% and 14.94% respectively, valued at approximately KES 17 billion and KES 19.3 billion. These politically connected shareholders add complexity to any acquisition negotiations.

Other Regional Players Positioning for Growth

FirstRand’s African Ambitions

FirstRand Ltd., Africa’s largest lender by market value based in South Africa, signaled in January 2024 that it is actively seeking acquisitions across African markets where it operates. Incoming CEO Mary Vilakazi indicated the bank would consider targets both within traditional banking and adjacent financial services, with East Africa identified as a key growth opportunity.

First Bank Nigeria’s Expansion Plans

First Bank of Nigeria announced plans in late 2024 to expand to at least three African countries starting in 2025, targeting Ethiopia, Angola, Cameroon, and the Ivory Coast. Deputy Managing Director Ini Ebong noted that the bank sees opportunities similar to those present in larger African markets in the early 2000s, though Kenya was not explicitly mentioned as a near-term target.

JPMorgan Chase’s Strategic Entry

In a surprise move, JPMorgan Chase received an operating license from the Central Bank of Kenya in October 2024, just days before CEO Jamie Dimon visited the country. The American banking giant’s entry, focused initially on government clients, large state enterprises, and multinationals, signals Kenya’s growing importance as a regional financial hub and may catalyze further international interest.

Dimon emphasized during his Nigeria visit that JPMorgan plans to add one or two African countries every couple of years, with Kenya serving as the East African anchor for traditional banking services to institutional clients.

The Pressure on Smaller Banks

As of December 2024, 12 of Kenya’s 39 licensed commercial banks held core capital below the KES 3 billion threshold required by December 2025. These banks collectively face a capital deficit of approximately KES 11.85 billion, creating immediate pressure to recapitalize, merge, or seek strategic buyers.

State-owned Consolidated Bank of Kenya faces the most significant challenge, requiring at least KES 3.5 billion to comply with the 2025 requirement. Other banks in the deficit category include UBA Kenya (KES 1.26 billion needed), Middle East Bank of Kenya (KES 956.93 million), Development Bank of Kenya (KES 856.93 million), Credit Bank (KES 544.66 million), and several others.

In July 2024, Stanbic Bank Kenya CEO Joshua Oigara predicted the new requirements would likely halve the number of banks operating in Kenya, echoing CBK Governor Thugge’s expectation of significant consolidation over the next five years.

However, the Kenya Bankers Association (KBA) indicated that mergers and acquisitions are unlikely in the first phase of compliance, as most affected banks can individually raise the initial KES 3 billion through capital injections from parent companies, rights issues, or retained earnings. KBA CEO Raimond Molenje noted that M&A activity would likely accelerate from 2026 onward as the capital threshold progressively increases to KES 5 billion and beyond.

What This Means for Local Banks

Kenyan institutions now face a strategic pivot:

| Option | Implication |

| Recapitalize | Expensive, especially amid high interest rates |

| Merge | Creates scale but involves complex integration |

| Sell | Immediate liquidity; risks loss of local control |

Foreign buyers offer capital, technology, and cross-border business linkages. Yet they also raise concerns about:

- Ownership concentration

- Profit repatriation

- Reduced local decision-making autonomy

The growing debate is whether the shift represents regional integration or foreign domination.

Winners, Losers, and Likely Outcomes

🔹 Potential Winners

- Consumers may enjoy better digital services and lower lending costs due to stronger funding bases.

- Corporate clients & SMEs gain access to cross-border finance.

- Fintechs partnering with larger banks benefit from scale.

🔸 Possible Losers

- Small local banks, squeezed by expensive capital raises.

- Employees, due to branch consolidation and restructuring.

- Local ownership advocates, worried about external control.

🔔 Likely Market Scenario by 2029

- Fewer banks, possibly 28–30 instead of 38

- Top five lenders controlling over 65% of market assets

- Foreign ownership crossing 55% of Kenya’s banking assets

Is This Integration or Domination?

The trend reflects a maturing African financial system. Unlike the 1990s and early 2000s—when global multinationals dominated—today’s consolidation is led by African banks buying African banks:

- Nigeria’s Access and Zenith Bank

- South Africa’s Standard Bank and FirstRand

This is regional integration driven by African capital, strategy, and ambition. Kenya is not losing its industry—it is becoming the continental battleground for banking supremacy.

The Road Ahead: Will Kenyan Banks Fight Back?

The true test lies in how local banks respond:

- Will they innovate faster than foreign rivals?

- Will mid-tiers merge to form stronger local champions?

- Will fintech partnerships preserve Kenyan competitiveness?

Some local banks may choose alliances, others defensive mergers, and a few may be absorbed. But one thing is certain:

Kenya’s banking map is being redrawn—and Africa’s powerhouses want in.

Strategic Rationale Behind the Consolidation Wave

Several interconnected factors are driving African banking giants toward Kenya:

Market Size and Growth Potential

Kenya remains East Africa’s largest economy and most sophisticated financial market, with a banking sector holding KES 7.5 trillion in total assets and serving a population of approximately 55 million. The country’s strategic position as a regional hub for trade, technology, and finance makes it an essential market for any pan-African banking strategy.

Regional Integration and Cross-Border Opportunities

Kenya serves as the gateway to the broader East African Community (EAC) market of over 300 million people. Banks with strong Kenyan operations can leverage this platform to serve multinational corporations, facilitate intra-regional trade, and capture cross-border payment flows. This regional dimension was emphasized in September 2025 when KCB Group and Afreximbank announced a $800 million funding partnership for the Vipingo Special Economic Zone, demonstrating the scale of infrastructure financing opportunities.

Digital Banking and Fintech Leadership

Kenya’s position as Africa’s fintech and mobile money leader, anchored by M-Pesa’s success, makes the market particularly attractive for banks seeking digital transformation. NCBA’s M-Shwari platform alone serves millions of customers, representing the type of digital infrastructure that foreign acquirers struggle to build organically.

Favorable Regulatory Environment

The CBK has demonstrated sophistication in managing the consolidation process, drawing on experience from the 2015-2016 banking crisis that saw the failure of Imperial Bank and Chase Bank. The phased implementation timeline for capital increases balances stability concerns with the need to strengthen the sector gradually.

In April 2025, the CBK announced it would lift the moratorium on licensing new commercial banks effective July 1, 2025, signaling confidence in the sector’s stability and creating additional competitive pressure that may accelerate consolidation.

Withdrawal of International Banks

The gradual exit of some international banks from retail and SME segments has created acquisition opportunities for African lenders. Standard Chartered’s divestiture of various African subsidiaries to Access Bank exemplifies this trend, with Western banks retreating to institutional banking while regional players expand retail and commercial operations.

Challenges and Risks

Despite the opportunities, several challenges confront African banks expanding into Kenya:

Asset Quality Deterioration

Kenya’s banking sector confronts significant asset quality challenges. The 16.7% non-performing loan ratio as of August 2024 represented an 18-year high, driven by economic headwinds, high interest rates, and delayed government payments to contractors. Private sector credit growth decelerated sharply to just 1.3% in August 2024, the lowest level in five years, constraining revenue growth opportunities.

Acquirers must carefully assess the NPL exposure in target institutions, particularly loans to government contractors and parastatals. The government’s fiscal challenges, including grey-listing by the Financial Action Task Force (FATF) in February 2024, add complexity to sovereign exposure risk management.

Integration Complexity

Integrating acquired banks across multiple African jurisdictions presents operational, cultural, and technological challenges. Banks must harmonize systems, align corporate cultures, manage redundancies, and maintain service continuity while extracting promised synergies. Access Bank’s experience integrating 14 acquired institutions across Africa will be tested as it absorbs NBK into its East African operations.

Regulatory Scrutiny

Cross-border acquisitions face multiple layers of regulatory approval, including competition authorities in Kenya and home countries, central bank approvals, and COMESA Competition Commission review for regional deals. The lengthy approval process for the Access Bank-NBK transaction, which required clearances from multiple authorities, illustrates these complexities.

Currency and Macroeconomic Volatility

Although the Kenyan shilling strengthened significantly in 2024, recovering from previous depreciation, currency volatility remains a risk for foreign banks repatriating profits or managing cross-border exposures. Inflation, while declining to 2.8% in November 2024 from 6.9% in January, could resurge if global commodity prices spike or fiscal pressures mount.

Political and Governance Risks

Kenya’s periodic political volatility, exemplified by the June 2024 protests that forced the government to withdraw a controversial Finance Bill, creates uncertainty for long-term strategic investments. Banks must navigate relationships with politically connected shareholders, as evidenced by the Kenyatta and Ndegwa family stakes in NCBA, while maintaining governance standards expected by international investors and home-country regulators.

Financial Performance and Valuation Considerations

The banking sector’s financial performance in 2024 provides context for acquisition valuations. Despite challenging conditions, major banks demonstrated resilience. Equity Group reported that regional subsidiaries contributed 51% of group profit before tax in FY2024, up from 50% the previous year, highlighting the importance of diversified geographic exposure.

KCB Group’s subsidiaries contributed 36.6% of group PBT, while the bank closed FY2024 with total assets exceeding previous years despite a 5% decline in net loans and advances. The sector maintained strong profitability with a return on equity of approximately 17% in the first half of 2024, despite a challenging operating environment.

Stanbic Bank Kenya reported a 15% increase in profit after tax to KES 13.7 billion for FY2024, demonstrating that well-capitalized banks can thrive even amid sector stress. The bank’s strong performance positions it well for the proposed NCBA acquisition, should Standard Bank proceed with the transaction.

NCBA’s consistent profitability and dividend track record make it an attractive target commanding premium valuations. The 38.5% share price surge following acquisition reports demonstrates investor confidence in the strategic value of the franchise.

📊 Timeline & Forecast: Kenyan Banking Consolidation (2023–2030)

Here’s a chronological chart of key regulatory milestones, projected deal activity, and market-impact phases — followed by a commentary on what each phase likely means.

| Period | Key Regulatory / Market Event | Forecasted Banking Market Impact |

| 2023 | – Early signals of pressure on weaker banks- Some banks already under-capitalised relative to forthcoming rules | – Preparatory activity by pan-African banks: scouting targets, initial due diligence- Emerging M&A discussions |

| Dec 2024 | – Business Laws (Amendment) Act passed, raising minimum core capital to KSh 10 billion by 2029. – Law becomes effective on December 27, 2024. | – Strategic shock: small and mid-tier banks scramble to plan recapitalisation.- Foreign and regional banks intensify M&A planning. |

| 2025 | – Minimum core capital must reach KSh 3.0 billion by Dec 31, 2025. – CBK issues final guidelines on capital, leverage, and funding ratios; deadline for compliance with new leverage, NSFR rules set at October 1, 2025. – CBK lifts the moratorium on issuing new commercial bank licenses effective July 1, 2025, but new entrants must meet the KSh 10 billion capital threshold. – By April 2025, 22 of 24 under-capitalized banks had submitted capital-raise plans; 2 requested extensions – People Daily | – First wave of consolidation among weak banks.- Some banks may seek strategic investors, mergers, or rights issues.- New-licence entrants face very high bar, limiting greenfield growth. |

| 2026 | – Capital requirement increases to KSh 5.0 billion by Dec 31, 2026 – Central Bank of Kenya | – Consolidation intensifies.- Several mid-tier banks may complete merger or acquisition deals.- Foreign banks (e.g., Nigerian, Egyptian) begin to close more deals, leveraging first-mover advantage. |

| 2027 | – Capital requirement moves to KSh 6.0 billion by Dec 31, 2027 – Central Bank of Kenya | – Further M&A among weaker players or forced exits.- Regional banks that entered early begin integrating operations, rolling out cross-border products. |

| 2028 | – Capital requirement rises to KSh 8.0 billion by Dec 31, 2028 – Central Bank of Kenya | – Mid-tier banking landscape has significantly consolidated.- Larger institutions (local and foreign) dominate; competition for scale peaks.- Customers benefit from improved balance sheets, digital upgrades. |

| 2029 | – Final phase: minimum core capital reaches KSh 10.0 billion by Dec 31, 2029 – Central Bank of Kenya | – Full compliance for most surviving banks.- Market structure likely has fewer but stronger banks.- Heightened cross-border banking integration; some foreign-owned institutions deeply embedded. |

| 2029–2030 (Outlook) | – Post-capital reform consolidation matures.- Regulatory landscape stabilizes.- Opportunity opens for greenfield banks (if they met capital) and fintech-bank hybrids. | – Stable, resilient banking sector with higher capital buffers.- Potential for more innovation (digital banking, trade finance, SME lending) driven by well-capitalised players.- Reduced risk of systemic shocks, but risk of concentration of ownership. |

🔍 Analysis: Phases & Strategic Inflection Points

1. Shock & Strategy (2024–2025)

- The passage of the Business Laws Amendment Act in December 2024 is the defining moment. That’s when the regulatory risk becomes real.

- Banks immediately begin scrambling to prepare capital-raising plans. As of April 2025, most had submitted plans to CBK – People Daily.

- Simultaneously, CBK’s rules on liquidity (NSFR) and leverage (Tier-1 to exposures) add more pressure — not just on capital, but on funding maturity – Tuko.co.ke.

- The lifting of the 2025 moratorium on new bank licenses (from 1 July) reopens the field — but new entrants face the same high capital requirement (KSh 10 bn) as incumbents.

2. Consolidation Acceleration (2026–2028)

- As the capital milestones increase (5 bn by end-2026, 6 bn by 2027, 8 bn by 2028), banks will find it increasingly hard to remain independent without scale or strong investors.

- We should expect a wave of M&A activity during this period — especially among second- and third-tier banks.

- Foreign banks (especially well-capitalized pan-African players) are likely to use this window aggressively. First movers may secure attractive deals before valuations rise further.

3. Maturity & Market Re-Structuring (2029)

- By end-2029, compliance with KSh 10 bn becomes mandatory. Many banks will have either transformed (through M&A), or risk being marginalized.

- The resulting system will likely have fewer but stronger banks — both homegrown and foreign-backed.

- Given this new stability, banks may shift to growth-oriented strategies: digital expansion, cross-border service, trade finance, and SME lending.

4. Post-Reform Dynamics (2029–2030 and beyond)

- Once the capital reform is done, the consolidation cycle may slow, but its effects will linger.

- New-licence entrants (post-July 2025) that managed to raise capital might increasingly challenge incumbents, especially if they target niche or digital-first segments.

- Strategic alliances (foreign-local, bank-fintech) could deepen: well-capitalized banks can invest in technology, and fintech players can plug into stronger deposit bases.

- For the broader economy, a more stable banking sector can absorb shocks better, support bigger lending, and drive regional trade flows.

✅ Key Takeaways from the Timeline

- Regulatory certainty matters: The phased capital increases provide both pressure and breathing room.

- Window of opportunity (2025–2028): This is when much of the M&A action will likely happen — a critical era for foreign banks to solidify their Kenya play.

- Long-term winners: Well-capitalized banks (local or international) with strong digital strategy and cross-border ambitions.

- Risks to watch: Over-consolidation (reduced competition), job losses, and foreign dominance concerns.

- Growth potential: A consolidated but well-capitalized sector could drive innovation, SME lending, and regional trade financing.

The Path Forward

Kenya’s banking consolidation wave represents a pivotal moment in African financial services, with implications extending far beyond national borders. The outcome will shape regional banking architecture for decades, determining which institutions emerge as true pan-African champions capable of financing infrastructure, facilitating trade, and supporting economic development across the continent.

For African banking giants, Kenya offers a unique combination of market depth, regional connectivity, digital sophistication, and regulatory clarity that makes expansion both strategically compelling and operationally feasible. The capital rules have created a time-limited window for acquisitions at potentially favorable valuations, before smaller banks complete recapitalization efforts or alternative strategic options emerge.

The CBK’s expectation of significant consolidation appears likely to materialize, though the timeline may extend beyond initial projections as banks exhaust alternatives to mergers. By 2029, when the full KES 10 billion capital requirement takes effect, Kenya may operate with 20-25 commercial banks rather than the current 38, with stronger institutions commanding larger market shares and serving regional rather than purely domestic strategies.

For investors, customers, and policymakers, the consolidation presents both opportunities and risks. Larger, better-capitalized banks should demonstrate greater resilience, offer more sophisticated products, and support bigger projects. However, reduced competition could pressure pricing and service quality, requiring vigilant regulatory oversight to protect consumer interests.

The influx of African banking giants into Kenya also marks a broader continental shift toward regional financial integration and reduced dependence on Western financial institutions. As Zenith Bank’s Henry Oroh articulated, the strategic vision involves creating African banking champions with sufficient scale to serve African businesses independently, reducing the need to seek financing from Western banks.

This vision of financial pan-Africanism, enabled by Kenya’s regulatory reforms and facilitated by the capital requirements catalyst, may prove the most significant legacy of this consolidation wave – the emergence of truly continental African banks capable of competing globally while serving African development priorities.